About the Authors

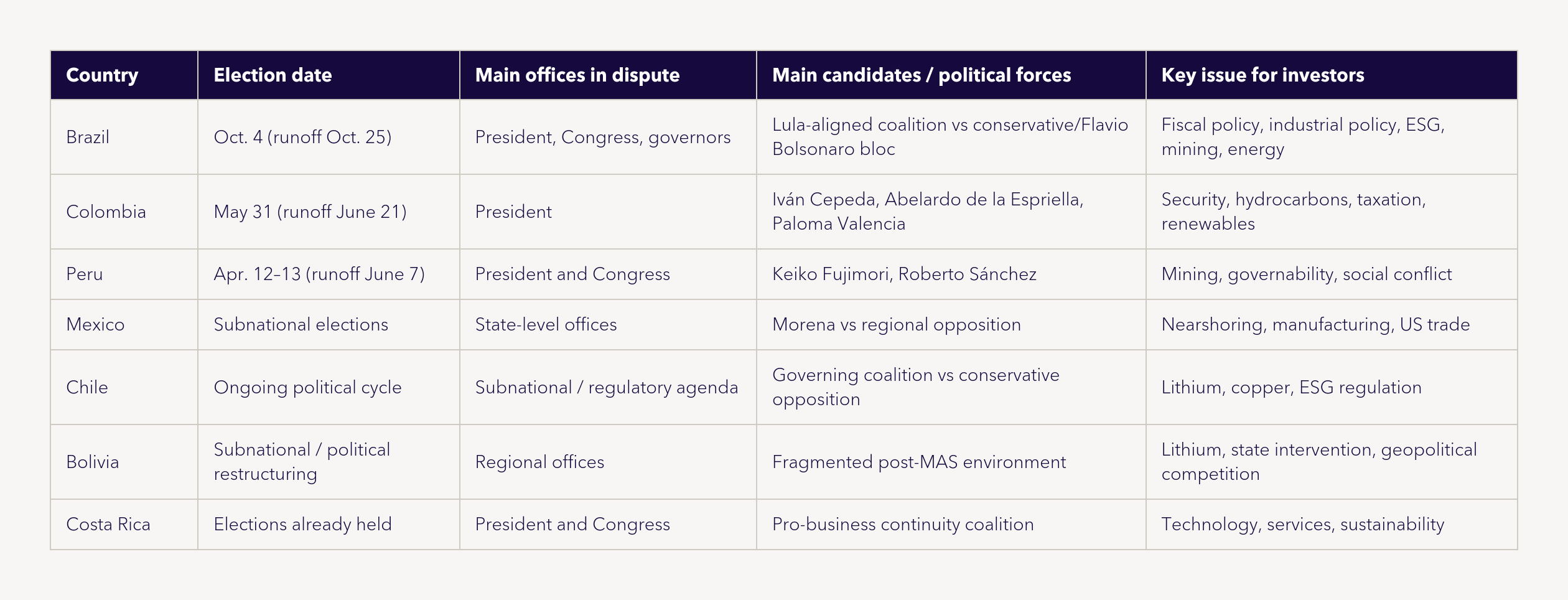

The 2026 electoral cycle is emerging as one of the most strategically significant political periods for Latin America in recent years. Presidential, legislative and subnational elections across the region are taking place at a moment marked by slower global growth, geopolitical fragmentation, pressure on public finances and intensifying competition for industrial investment linked to energy transition, critical minerals and nearshoring.

Unlike previous electoral cycles primarily shaped by ideological polarisation, the current regional environment is increasingly defined by governance capacity, economic security and institutional resilience. Questions surrounding inflation, public security, industrial policy, energy transition and state intervention are now directly influencing investment flows and business confidence throughout the region.

For multinational corporations and investors, the implications extend well beyond electoral outcomes themselves. The broader challenge lies in navigating fragmented political systems, rapidly evolving regulatory agendas and growing social pressure around ESG, inequality and local economic development.

In practice, Latin America is entering a phase where politics, geopolitics and business strategy are becoming deeply interconnected.

Colombia: a narrow mandate, ideological shift and the return of orthodoxy

Colombia concluded its 2026 electoral process with a highly contested presidential runoff on June 21, resulting in the victory of Abelardo De La Espriella. Following a historically tight race against left-wing candidate Iván Cepeda, De La Espriella secured the presidency with a margin of less than 1%, marking the narrowest gap in percentage terms since the introduction of runoff elections in 1994. The election also saw a record-breaking voter turnout, exceeding 63% of the electoral register.

Beyond the existence of transition meetings, the De La Espriella team’s confidence in the information being handed over, together with the government’s lack of willingness to facilitate the incoming team’s work, makes it foreseeable that the process will not be smooth. That said, it is clear that the incoming government will undertake a thorough audit allowing it to build a rear-view mirror of the pressing challenges it faces in areas such as healthcare, energy security, public safety and the fiscal deficit.

The results confirm the emergence of a new two-party system in Colombia, defined by deep territorial, identity, and ideological divisions. De La Espriella represents a new right-wing force that transcends traditional Uribism, merging a strong stance on security with the banners of anti-politics and the recognition of necessary social transformations. Conversely, the Pacto Histórico has consolidated itself as the country’s leading political force and is expected to lead a staunch, confrontational opposition through Congress, social movements, and the media.

The challenge for Colombia’s institutions under this scenario is to make progress in resolving the country’s main economic and social problems within a government–opposition framework whose defining feature will be confrontation. The traditional parties (Conservative, Liberal, the U Party) may serve as a hinge to secure majorities in Congress, but tensions will persist in other arenas:

- Public order: blockades and demonstrations

- Labor: union matters

- The judicial sphere

- The proposal for a constituent assembly

The above means that Abelardo De La Espriella’s victory guarantees the private sector neither legal certainty nor an optimal social environment in which to operate. What it does generate is a greater capacity for dialogue with the national government, as well as the possibility that, at least temporarily, economic growth will prevail over other considerations in decisions on security, taxation and permits/licenses. For investors, the incoming administration signals a return to macroeconomic orthodoxy in managing debt, inflation, and central bank relations, along with a sharp geopolitical pivot back toward Washington.

Key considerations for companies and investors

- De La Espriella aligns Colombia with Latin America’s rightward shift (Argentina, Chile, Bolivia, Paraguay and Ecuador) and triggers a sharp pivot back toward Washington after the Petro years. Trump and Republicans quickly congratulated De La Espriella, and analysts expect closer cooperation on security, migration, and trade, plus a reshaped stance toward Venezuela and other neighbors.

- The elected president stated that during his term he will turn embassies into commercial agencies to attract foreign investment into the country.

- The clearest winner sectors under De La Espriella are oil, gas and mining. He pledges to revive exploration, pursue fracking, develop metals and rare earths, and create tax-exempt special economic zones. Infrastructure and construction, housing and banking, agribusiness, defense and security, tourism, and tech also stand to gain, with broad upside for the private sector from lower corporate taxes and deregulation. Markets have already reacted, with the dollar hitting six-year lows.

- The caveat: execution is the real test. Much of the optimism is already priced in, foreign investment in oil and mining has been weakening, and a narrow mandate plus inflexible public spending limit the fiscal room to deliver on these promises.

Brazil: fiscal credibility, industrial policy and strategic positioning

Brazil’s general elections will take place on October 4, 2026, with a possible runoff scheduled for October 25. Voters will elect:

- President;

- National Congress (all 513 representatives and 2/3 of the Senate);

- all (27) state governors;

- and state legislatures.

The election is widely expected to become the region’s most consequential political event from an economic and geopolitical perspective. Brazil combines continental scale, strategic natural resources, industrial capacity and growing relevance in global discussions surrounding energy transition, food security and critical minerals.

The political landscape remains highly polarised. President Luiz Inácio Lula da Silva is expected to seek another term, while the conservative opposition continues reorganising around the broader Bolsonaro political movement, with Senator Flavio Bolsonaro, son of the former and imprisoned president Jair Bolsonario, on the ballot. Polling scenarios currently suggest highly competitive dynamics between Lula-aligned candidates and conservative forces associated with former president Jair Bolsonaro and his allies.

Beyond the cultural wars, central debate increasingly revolves around:

- fiscal sustainability;

- industrial policy;

- environmental regulation;

- digital governance;

- public security;

- and Brazil’s geopolitical positioning between the US, China and Europe.

Investors are paying particular attention to the continuity or potential redesign of initiatives such as Nova Indústria Brasil, the federal government’s industrial policy framework focused on reindustrialisation, infrastructure, energy transition and strategic sectors.

Brazil’s growing role in global supply chains also places mining, infrastructure and ESG regulation at the centre of the political debate. The country is increasingly positioning itself as a strategic supplier of biofuels, agricultural commodities, rare earths, nickel, graphite and other minerals required for advanced manufacturing and energy transition industries.

At the same time, investors remain cautious regarding:

- fiscal trajectory;

- regulatory predictability;

- tax reform implementation;

- environmental licensing;

- and broader governability risks in an increasingly fragmented Congress.

Key considerations for companies and investors

- Fiscal credibility and industrial policy continuity will be central market drivers after the election.

- Mining, energy transition, infrastructure and agribusiness are likely to remain strategic sectors regardless of the electoral outcome.

- ESG, Amazon-related policies and environmental licensing will continue shaping Brazil’s global positioning and access to capital.

- Political fragmentation may complicate structural reforms even under a market-friendly administration.

- Government affairs, regulatory monitoring and stakeholder engagement will remain essential for companies operating in strategic sectors.

Peru: institutional instability and strategic mining relevance

Peru held the first round of presidential and legislative elections on April 12–13, 2026, followed by a highly contested runoff on June 7. All congressional seats were also renewed, including the return of a Senate chamber for the first time in decades, which resulted in a fragmented bicameral Congress characterized by the absence of an absolute majority.

The country entered the election cycle after years of institutional instability, presidential removals and escalating political fragmentation. Since 2018, Peru has experienced repeated presidential crises, congressional confrontations and widespread social unrest, severely undermining confidence in political institutions.

The presidential contenders in the runoff resulted in a virtual tie, reflecting a deeply divided electorate. The final resultis expected to take weeks to be consolidated due to the manual counting of votes, but:

- Roberto Sánchez, associated with the left and supported by sectors aligned with former president Pedro Castillo, currently holding a razor-thin lead with approximately 50.07% of the votes.

- Keiko Fujimori, representing the conservative Fujimorista political tradition, closely trailing with 49.93% of the votes as the electoral authority finalizes the tally of rural and contested ballots.

The election matters globally because Peru remains one of the world’s largest copper producers and a strategically important mining jurisdiction for energy transition supply chains. Copper demand linked to electrification, renewable energy infrastructure and EV manufacturing continues to grow rapidly.

For investors, however, Peru increasingly presents a paradox due to its exceptional geological potential, but persistent political and social instability. Community conflict surrounding mining projects has intensified in several regions, while operational disruptions, anti-mining activism and institutional distrust continue affecting project timelines and investor confidence. The delayed election results and extreme political polarization add further layers of uncertainty.

Still, Peru retains important competitive advantages:

- strong mining expertise;

- strategic Pacific connectivity;

- and substantial mineral reserves critical to global industrial transformation.

Key considerations for companies and investors

- Political volatility and weak institutional coordination remain major investment risks.

- Copper and mining projects will continue occupying a central role in Peru’s economic model regardless of the electoral outcome.

- Social conflict and community relations are increasingly decisive factors for operational viability.

- Mining-friendly candidates currently dominate much of the electoral field, reducing the likelihood of abrupt anti-market shifts.

- Infrastructure, logistics and Pacific trade connectivity remain long-term strategic strengths.

Other relevant political developments across the region

Although Brazil, Colombia and Peru dominate the regional political calendar, several other electoral and political developments remain highly relevant for investors.

In Mexico, despite the presidential election having taken place in 2024, important state-level elections and broader political developments will continue shaping nearshoring, manufacturing and industrial investment conditions. The country remains highly exposed to US trade policy, tariff disputes and industrial competition linked to US-China tensions.

Chile started a new political cycle still debating mining governance, lithium policy and environmental regulation, all highly relevant for global copper and battery supply chains.

Bolivia remains strategically important due to its lithium reserves and growing geopolitical relevance in global battery and energy transition discussions. Political fragmentation and state intervention continue affecting investor confidence.

Costa Rica, which already held elections earlier in 2026, continues consolidating its position as a relatively stableregional hub for technology, medical devices and sustainable investment.

Navigating a more complex Latin America

This said, Latin America’s 2026 electoral cycle arrives at a moment of profound global transformation. The region is increasingly positioned at the intersection of critical global trends involving energy transition, industrial reconfiguration, geopolitical competition and supply chain resilience.

Across the region, the challenge for governments will be balancing economic growth, fiscal stability, environmental pressures and social expectations within increasingly fragmented political environments. For companies and investors, navigating Latin America will require far more than macroeconomic analysis alone. Political intelligence, stakeholder engagement, regulatory monitoring and reputational management are becoming core business functions rather than peripheral considerations.

SEC Newgate supports organisations operating across Latin America through integrated capabilities spanning public affairs, geopolitical analysis, strategic communications, stakeholder engagement and risk anticipation. As political, regulatory and societal dynamics become increasingly interconnected, coordinated regional strategies and deep local insight are becoming essential competitive advantages for companies operating in complex and highly regulated markets.